Living From Capital : The Basic Maths

Why a Safe Withdrawal Rate is like a Magic Steak

Imagine you had a magic steak where you could eat a piece…and it could then grow back.

That piece of steak could feed you*. And, as long as you don’t cut too much off the steak each time, it will regrow and feed you again in the future.

You can keep living off the steak indefinitely and it should never run out.

* p.s. This is not a diet recommendation, it’s an analogy to illustrate a point!

This is a bit like the maths of living off capital.

The investment portfolio is the steak. You sell some units from your portfolio each year and live off the proceeds. The investment portfolio then, if all goes well, regrows the amount that you spent. Some years more, some years less.

This works if your portfolio is large enough (and your spending is low enough). If so, you could live from the investment portfolio and the investments will regrow the money that you spent on your groceries and other bills.

It’s good to have a rough idea of what amount money you would need to live from capital.

You might be retired with a pot of investments (but no defined benefit pension scheme) to live off. You need to understand how much you can safely afford to drawdown and spend each year.

Or you might just want to know how much wealth gives you the option not to work.

Or how much wealth covers your basics (e.g. groceries and utility bills) leaving you free to spend earned income on holidays / luxuries etc.

According to the basic maths of financial independence, you can safely eat some percentage (let’s say ~4%) of The Magic Steak each year.

In other words, you can spend say ~4% of the initial balance of a retirement portfolio and then increase that by the rate of inflation for the rest of the retirement period.

So someone starting retirement with a £1 million pot can spend ~4% (£40,000 per year rising with inflation) and probably never run out of money.

We don’t need to argue here about whether the much-discussed “safe” withdrawal rate is actually 4.25% or 3.25% or whatever. We’ll get to that later in the article. For now, I’m just illustrating the concept.

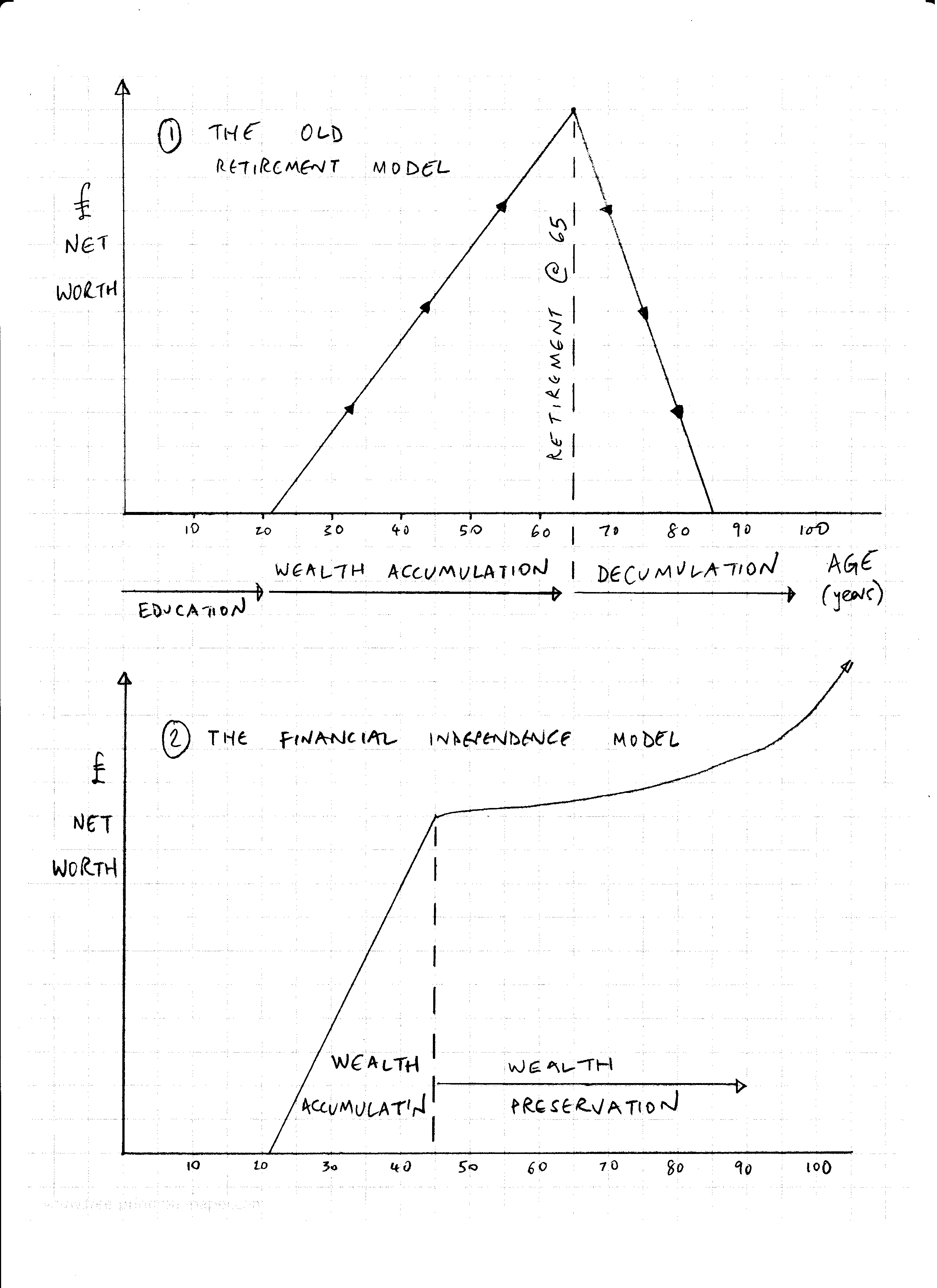

It’s hard to do complex financial modelling in your head.

So people often think about retirement drawdown as a linear decrease in wealth. In other words, if a retiree starts with a cash pot of £1,000,000 and spend £50,000 a year, then the money will last 20 years. This is obviously too simplistic because it ignores investment returns and inflation.

The simplistic (linear) model of drawdown looks like the top half of the figure below:

Now let’s add in investment returns and look at the second model.

The second model - the financial independence model - is like The Magic Steak.

Here wealth can continue to grow…even after retirement. If you spend 4% a year from the initial balance and you get equity investment returns of 5 - 7% a year (in real terms, inflation adjusted), then the pot is going to keep growing even during retirement / drawdown.

In reality, that smooth-looking upward curve in the wealth preservation phase will have lots of wiggles up and down due to the natural volatility of the stockmarket. What you get is a rollercoaster ride of multi-year bull markets and the occasional nasty bear market.

There are no guarantees. But the caution built into the modelling of safe withdrawal rates mean the most likely outcome will be dying with more money than the retiree had at the start.

If someone is aiming to “Die With Zero” then withdrawal rates significantly higher than 4% could be justified.

We can turn an assumed 4% Safe(ish) Withdrawal Rate on its head to calculate how much is enough.

The 25x Rule of Thumb says that you will probably have enough to live on sustainably when you have a pot of invested net worth of 25x your annual required spending.

This 25x is just the inverse of a 4% safe withdrawal rate (100 / 4 = 25).

So someone starting with a £1 million pot can spend 4% (£40,000 per year rising with inflation) and probably never run out of money. £40,000 x 25 = £1,000,000.

The numbers can be scaled up or down. If you spend £20,000 per year, you need an investment portfolio of £500,000. But if you spend £80,000 per year, you need an investment portfolio of £2,000,000.

In the real world, we have taxes. In the UK, drawings from a pension are subject to income tax for amounts above the £12,570 personal allowance.

You can take account of income tax by including it as part of your projected spending. So if you withdraw £40,000 from a UK pension and pay 20% basic rate tax of £8,000, that leaves you £32,000 for real spending.** I’ve ignored the £12,570 personal allowance here for simplicity

We also have a state pension (currently £12,547 per year for full pension) that can be factored in as negative spending.

So you’ll need to consider your own individual situation and you might want to model it out with a spreadsheet (one of the things I help my financial coaching clients with is reviewing financial models).

I’m not advocating anyone quit their job based solely on a rule of thumb!

Believe it or not, the MSCI-World equity index has compounded at 13.2% annualised over the past 10 years. That feels high. It’s higher than the longer term returns for global equities between 1900 - 2025.

And the starting point matters. The Shiller price : earnings ratio is currently over 42x and approaching the 44x seen at the top of the dotcom boom in 2000.

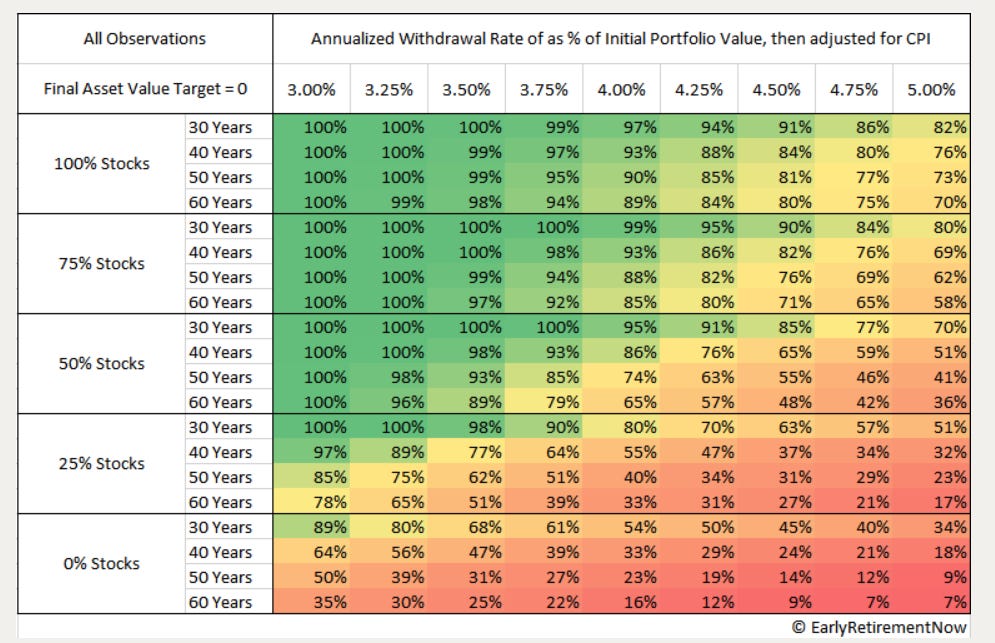

Sequence of returns risk is the risk of bad investment returns in the early years of retirement. The problem comes when you have to sell too many units (at low prices) to fund your living costs in the early years.

It is the early years of retirement which are dangerous for portfolio survival rates (aka running out of money later in life).

The key controllable factors influencing our chances of success (not running out of money) are:

the % withdrawal rate;

how the money is invested (the asset allocation);

the duration of the retirement period.

Let’s summarise the impact of these using the excellent work in The Safe Withdrawal Rate Series at Early Retirement Now.

The percentages in the table show the % of historical time periods when the portfolio would have out-lasted the retiree:

Safety is like beauty: it’s in the eye of the beholder.

What is your definition of safe? A 4% withdrawal rate with a 30 year retirement had a success rate of 99% using an asset allocation of 75% US equities : 25% US bonds.

Finally, a simple illustration of the mechanics of living off capital.

If global equities deliver say 10% per year, remember that is a total return that comes in two parts: income and capital.

To illustrate, imagine a rental house with a 5% rental yield and a 3% annual capital growth. That delivers you a total return of 8% per year on a buy to let property.

Well, it’s very similar with equities. Overall, the returns from the stockmarket have historically been better than property (a bit better in the UK, a lot better in the USA).

You tend to get a bit less in dividend income (versus property) and a bit more of the return from capital gains. So we might expect a ~10% total return from equities to be made up of 2.5% of dividend return in year one with an average expectation of 7.5% of capital gain per year.

If a retiree is planning £40,000 per year to live off they can fund this through a mixture of dividend income plus selling some units.

If the dividend yield is 2.5% on our investment portfolio of £1,000,000, then our portfolio will generate £25,000 of dividend income per year. So they sell £15,000 units of the fund each year to raise the cash to take them up to the £40,000 per year that they plan to spend.

If you invest in income paying exchange traded funds (ETFs) such as VWRL (The Vanguard All World Equities ETF), then the dividends are typically paid out as cash quarterly throughout the year.

A summary of how to live off capital.

You will need:

A home with the mortgage paid off;

An investment portfolio of >25x your required spending (incl. tax);

Something to do that provides structure, meaning and purpose

Obviously you could rent in retirement but living mortgage free means no exposure to rising interest rates. It locks in a lower cost of living and is easier to plan and calculate your base level of required spending.

There is a lot more to the decision of when (and whether) to quit a job (or career) than just the financial aspects.

It’s very powerful to keep working and earning after you have reached financial independence. Continuing to work and earn income after reaching financial independence is a super-power. It means you don’t have to sell units…so no sequence of returns risk.

This is not just a financial question. In my financial coaching, I encourage people to explore other options rather than just run straight to early retirement. To look for a new path in life that provides positive “towards” motivation.

A new job, consulting gig or a small business helps you structure your time. And it should provide structure, meaning and purpose.

Evolution is better than revolution.

Barney

Please hit reply if you’d like to talk about financial coaching or career coaching

You can set up an introductory call with me here.