The Aggregation of Marginal Gains (revisited)

and the advantages of consistency

The disadvantage of having written a blog for 10 years is that you get to be embarrassed by your earlier stuff.

But one of my early foundational articles that still works well almost a decade later is The Aggregation of Marginal Gains.

The basic idea is that it all adds up. Every financial decision that you make aggregates and compounds over time. You get to financial independence the same way you eat an elephant: one bite at a time.

I recently updated this article to add some extra content, some extra nuance and some extra graphs and pics that bring it to life.

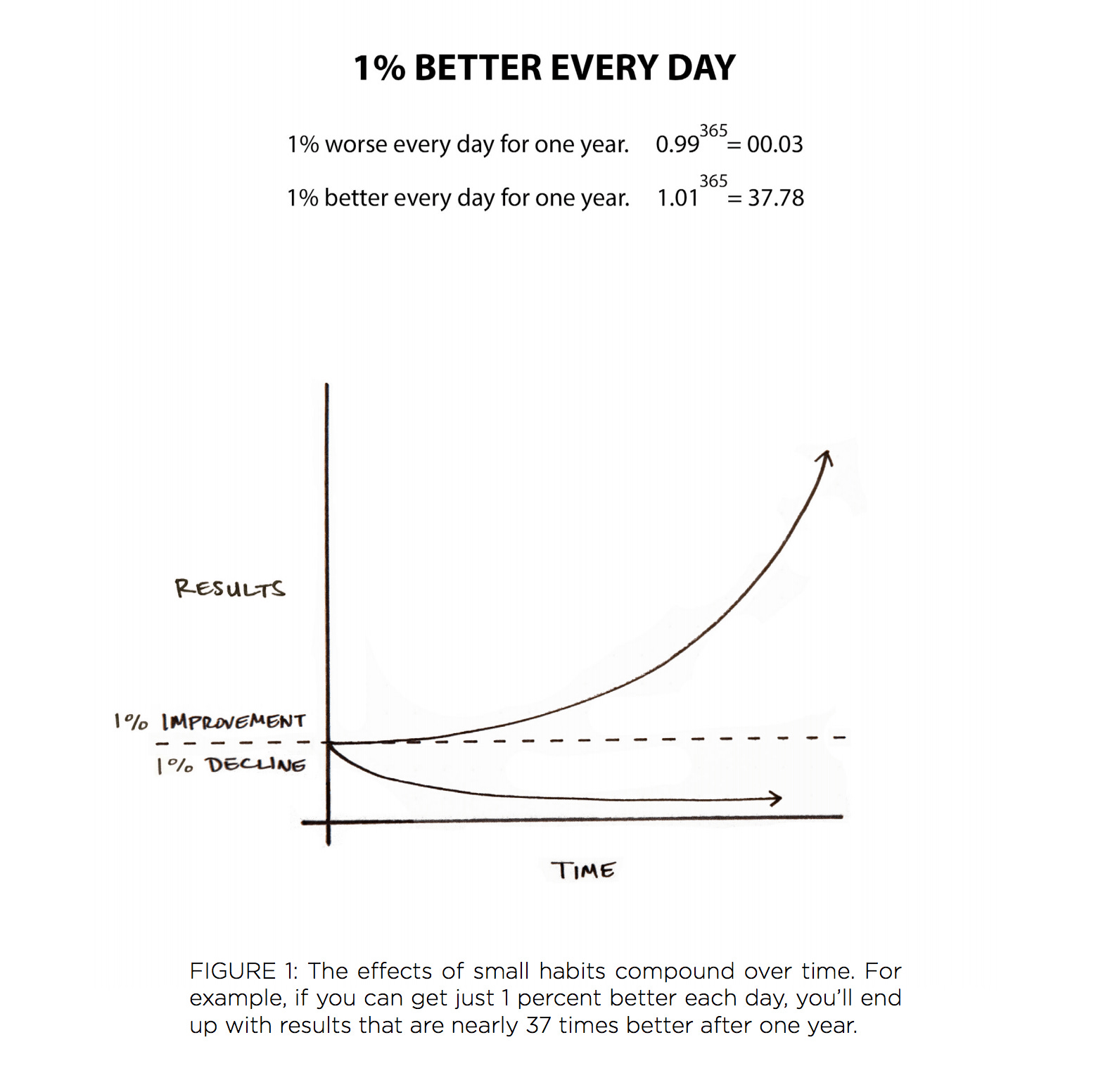

Take this graph for example which explains so much:

The gap between the two arrows is what is popularly referred to as “inequality of outcome”.

If you are in the wealth-building game, you are in the business of creating diversity of outcome.

You may not be seeking inequality of outcome per se but if everyone else around you is broke / financially retarded / living paycheck to paycheck, well then you need MORE inequality of outcome not less.

Journalists and left wing politicians bang on about inequality of outcome, hoping we all just assume it’s a bad thing. They hope the audience won’t spot the sleight of hand and won’t be able to tell the difference between i) inequality of opportunity and ii) inequality of outcome.

But they ain’t the same ting. Not at all. If people have freedom to make different choices, different outcomes are guaranteed. The more different the choices, the more different the outcomes.

When I started blogging, I didn’t fully appreciate the difference between i) just being a blogger online and ii) doing financial coaching with real people in the real world.

If you are just a blogger or Youtuber, the incentive is to push “TRY THIS ONE SIMPLE STRATEGY FOR GUARANTEED SUCCESS” type messages. The algorithm rewards the extremes rather than nuance.

But as soon as you focus on helping real people solve money-related problems in the real world, you realise that everyone is different and you have to meet people where they are.

Since then I have stopped trying to “sell” or “push” financial independence or early retirement on anyone else.

I don’t even think early retirement is necessarily healthy…certainly not for everyone. I think you can win the game by having financial security (debt free + emergency fund) plus finding a way to get paid to do something that gives you meaning, purpose and challenge.

All money does is to enable and de-risk the lifestyle that you want. The more runway you have, the safer you are.

I say “All money does”…as if it’s no big deal…

…but it’s actually a REALLY big deal. It’s fine to stop focusing on money once you have solved all your money problems. But until then, you probably need to focus on money.

Plugging away at consistency

I am focussed on consistency at the moment.

If you are headed in the wrong direction, then consistency is a disaster. You need discontinuity, you need disruption, you need change.

It’s fascinating how often people say that a shock or personal crisis (eg losing your job) eventually turns out to be a blessing in disguise. I applaud the reframe and the positivity but it’s also an admission that they were previously heading in the wrong direction.

If however you are pointing in roughly the right direction, consistency becomes a super-power.

I am coming up to one year without alcohol. I don’t know whether this is right for anyone else but I know it’s been right for me. It’s helped me stay pointing in the right direction despite whatever chaos might be going on elsewhere in my life.

Everyday I write my new AF number (today is day 357) in my journal.

And everyday I write something or add something or improve something in my financial coaching / financial education micro-business.

Eventually the metrics tell you whether it’s working or not:

Love to everyone

Barney