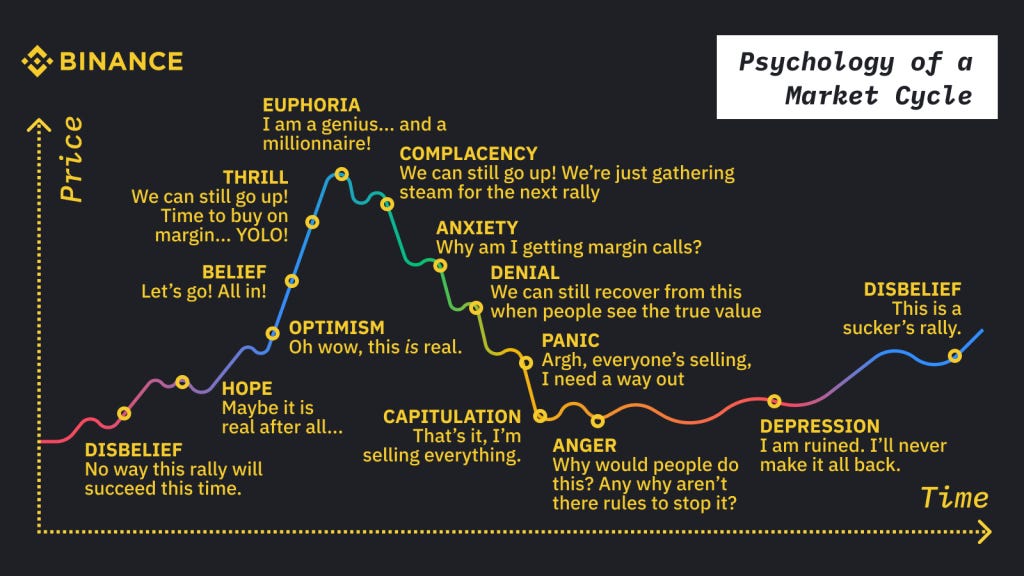

The Bubble Edition

If that stockmarket is so efficient, how are bubbles even possible?!?

There is much debate currently over whether we are in another tech bubble like 2000.

The Shiller PE ratio is certainly back in that valuation territory:

I won’t rehash those arguments here. For most people saving for retirement etc, the best thing to do is to keep calm and carry on investing each month.

In some ways, the more interesting question is: if markets are efficient, how is it even possible for bubbles to form?

If all the institutional investors that dominate the market are sane, smart and rational, how can we end up with crazy bubbles?

One answer is that bubbles form because not everyone in the stockmarket is playing the same game.

To illustrate, imagine a simplified world where there are 2 types of active player in the stockmarket following two different strategies:

Value-conscious investors

Momentum traders

[We add index fund investors as another category below…]

Both value investors and momentum traders are picking stocks to buy and sell. Both are making active (and in their mind rational) investment decisions.

But the value investors and the momentum traders make their decisions using very different systems. Their two strategies are as different as chalk and cheese.

Value investors

The value-conscious investors seek to buy when prices of individual companies are below fair value based on fundamentals. They sell when stock prices are overvalued.

Value investors like fundamentals: things like earnings, cashflow, dividends etc. In the old days, they used to like asset-backing.

Even investors in high-growth stocks consider whether the expected growth justifies the price. So these growth investors are also value-conscious.

Value conscious investors consider themselves rational (as we all do) but they think of the momentum traders as crazy gamblers.

Momentum traders

In contrast, the momentum traders don’t look at valuations; they don’t even need to know anything about the company.

For momentum traders, “the trend is their friend”. They are trend-followers who study price charts (technical analysis), buy on strength and sell on weakness.

In this trading system, price increases are a buy signal because they convey information, either about the improving prospects of the company and / or growing interest from other market participants.

And price falls are a sell signal. Momentum traders are flightier than the value investors. They set stop losses to get out early if prices start to fall.

You can think of the market as a balancing act between these 2 very different types of investor.

In a rising market, momentum traders will buy more shares from the value investors (and sell more shares to them in a falling market).

Individual mutual funds can have inflows and outflows but the stockmarket as a whole can not. Every security must be held by someone. Buyers must be matched with sellers, so prices adjust to match demand with supply.

Every time a new buyer enters the stockmarket, the share that they buy must be sold by someone else.

From this perspective, what matters is not the balance between bulls and bears per se, but the balance of sentiment between trend-sensitive and value-conscious investors.

Different investment styles explains why a crazy bubble market like the late 1990s tech boom can happen…and persist for longer than people think.

Here’s how a bubble plays out:

Companies in a “hot” sector release positive news and earnings surprises. This catches attention from analysts, investors and traders. Stock prices start to move up and this attracts momentum traders. Prices rise to encourage some value investors to sell.

This pattern could be reflexive (self-reinforcing). If prices continue to rise, momentum traders report out-performance. Fund investors tend to invest in strategies that have been out-performing recently. So new capital will tend to flow to those institutions following momentum strategies.

Bubbles can grow as long as more momentum traders keep buying on strength. The momentum traders are not worrying about valuations, they just follow their system and ride the trend.

Whilst momentum traders are accumulating, value-conscious investors are selling.

This goes on until some sort of tipping point is reached, a bit like how adding sand to a sandcastle eventually causes a collapse.

There could be an external shock (i.e. bad news) but market crashes don’t need bad news. Price stagnation could be enough to provide the tipping point. As momentum stops, some of the momentum traders pull out.

This triggers a collapse. Sharp declines happen when momentum traders try to exit en masse after being “all in”. Stop losses get triggered.

Any use of leverage makes it worse. A 3x leveraged ETF gets wiped out by a 33% fall. Margin calls must be met or positions get liquidated.

Value investors who have been sat on the sidelines wait. They require big price drops to induce them to invest. The pendulum swings from over-valuation to under-valuation.

The cycle can then repeat.

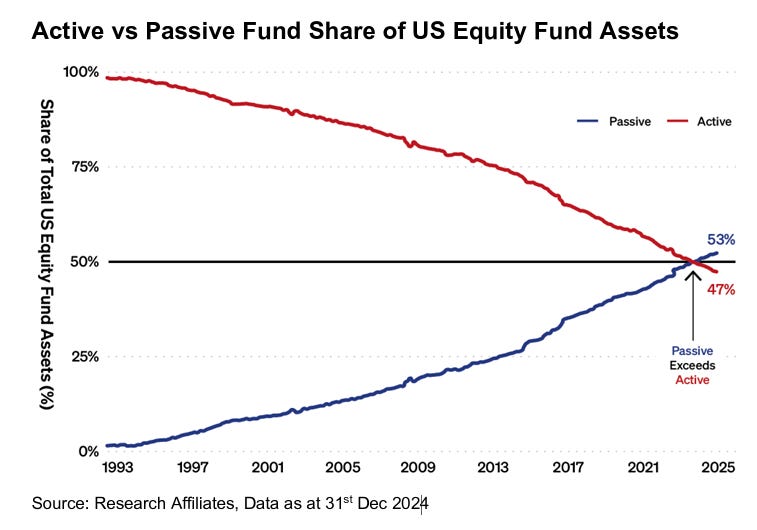

Now let’s introduce a third category of market participant: index funds.

Index funds are passive and do not use judgement to assess valuation or technical analysis to assess momentum. So you can’t put them neatly into either the value investor category or the momentum trader category. But they are more similar to the momentum traders than to value investors.

Index funds hold the companies in the index that they are tracking (e.g. MSCI World). Index funds are then rebalanced periodically to track the make up of the relevant market index. They add more of the “hot” stocks that enter the index and they sell the laggards leaving the index.

So rising ownership by index funds will tend to push the market in the same direction as momentum traders, especially if some value investors switch to a passive index-tracking strategy over time.

Index funds have been winning market share ever since their invention in the 1970s.

In the last couple of years, a milestone has been reached whereby passive index funds are thought to have gained more market share than actively managed funds. This crossover point is shown below:

Is this a problem?

Jack Bogle, the pioneer of index investing who founded Vanguard, the index fund manager, was asked at the 2017 Berkshire Hathaway annual meeting if there was a level of assets in index funds which would distort markets and he agreed that there was, although he had no way to know that level.

The design of index funds forces them to follow a momentum strategy of sorts. As a stock like Google becomes more valuable and enters the index, index funds are required by their design to buy it and match its growing index weighting.

The “Magnificent Seven” (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta and Tesla) currently make up roughly 35% of the S&P 500 by market-cap weight and growing.

All this is relevant today as the US stockmarket has made new highs amidst an AI investment boom.

The “winner-takes-all” network effects in information technology are greater than in past eras.

Index funds tend to reinforce the momentum traders. Buying by active traders leads to buying by passive investors. Buying begets more buying.

Index fund investing is a good thing. It’s the simplest and most efficient way for most people to invest for retirement etc.

But bubbles have been a fact of life all through history, from tulips to tech stocks. And we can’t rule out the possibility that the rise of index investing is contributing to the creation of bigger bubbles.

Let’s be careful out there!

Barney

One-to-One Coaching

If you’d like to discuss one-to-one financial or career coaching...

→ Email me on: barney.whiter@gmail.com

or